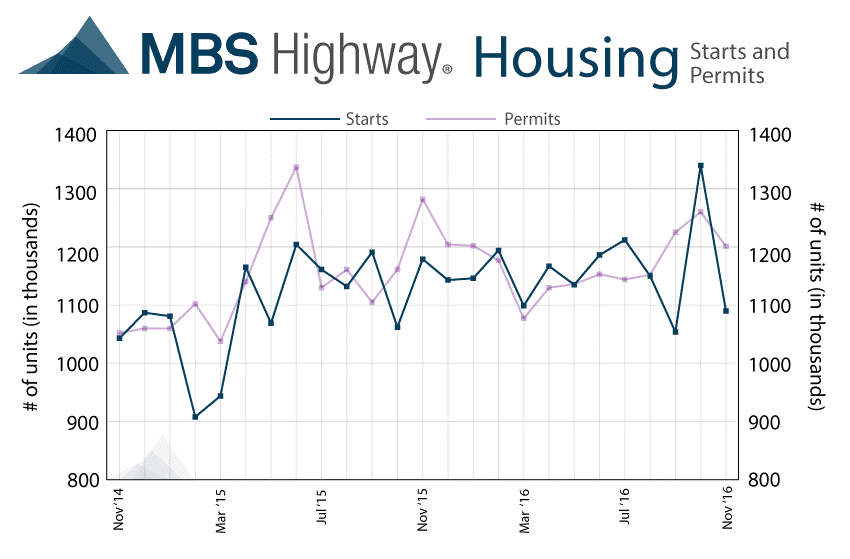

This past week the major stock market indexes ended mixed for the week while bond prices plunged, with yields and interest rates rising. The week’s most significant piece of economic news was the Federal Reserve’s decision to raise the target for the fed funds rate by 25 basis points to a range of 0.50 – 0.75%. While this rate hike was widely anticipated, the financial markets were surprised by the Fed signaling their intention to raise rates an additional three times in 2017 which was higher than market expectations for only two rate hikes next year. This forward guidance on interest rate hikes sent a strong hawkish signal to the bond market, sparking a sell-off in Treasuries and mortgage bonds while strengthening the U.S. dollar. Selling in the 10-year Treasury note pushed yields to 2.599% on Friday to its highest level since September 2014 while the U.S. Dollar Index soared 1.3% to its highest mark since early 2003. As for mortgages, the Mortgage Bankers Association (MBA) released their latest Mortgage Application Data for the week ending December 9 showing the overall seasonally adjusted Market Composite Index fell 4.0%. The seasonally adjusted Purchase Index declined 3.0% from the prior week, while the Refinance Index fell 4.0%. Overall, the refinance portion of mortgage activity increased to 57.2% of total applications from 56.2%. The adjustable-rate mortgage share of activity accounted for 6.2% of total applications. According to the MBA, the average contract interest rate for 30-year fixed-rate mortgages with a conforming loan balance increased from 4.27% to 4.28% with points decreasing to 0.36 from 0.37. In housing, the Commerce Department reported Housing Starts fell more than forecast in November, dropping 18.7% at a seasonally adjusted annual rate of 1.09 million versus a consensus forecast of 1.225 million. However, the rate of Housing Starts in October was revised higher to 1.340 million from 1.323 million. Meanwhile, Building Permits declined 4.7% at an annual rate of 1.201 million while the consensus forecast had predicted a decline of about 1.6% to a rate of 1.236 million. October’s Building Permits were revised higher to an annual rate of 1.260 million from 1.229 million.

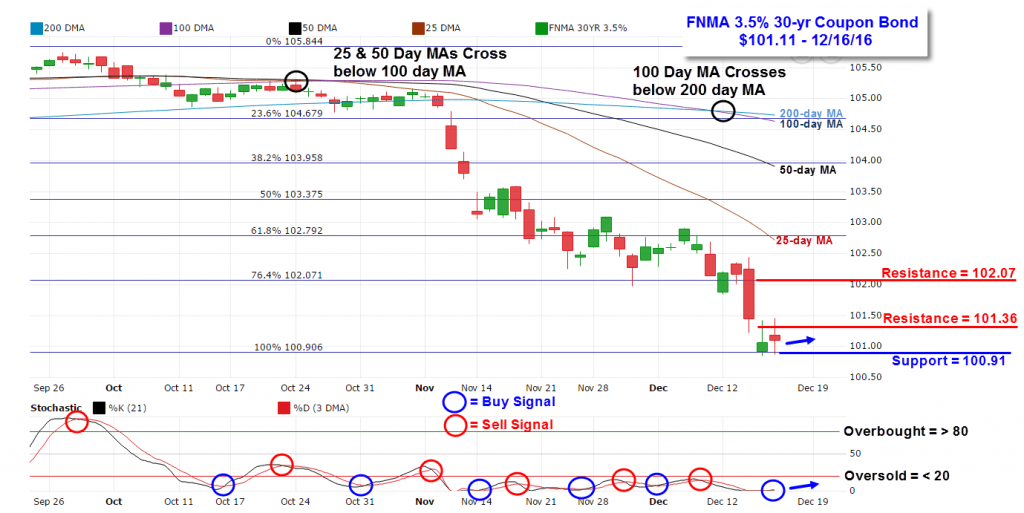

Mortgage Rate Forecast with Chart FNMA 30-Year 3.5% Coupon Bond Bond prices edged higher on Monday and Tuesday only to plunge on Wednesday and Thursday before recovering slightly on Friday. The FNMA 30-year 3.5% coupon bond ($101.11, -103.2 basis points) traded within a wider 160 basis point range between a weekly intraday high of $102.44 on Wednesday and a weekly intraday low of $100.84 on Thursday before closing the week at $101.11. Friday the bond bounced marginally higher off of the 100% Fibonacci retracement support level located at $100.91. Nearest overhead resistance is found at $101.36 while stronger resistance is located at the 76.4% Fibonacci retracement level at $102.07. Overall, the bond chart shows significant technical damage has taken place since the end of September, and especially since stock prices have rocketed higher in response to the presidential election. The black circles on the chart show multiple negative moving average crossovers. Although these are “lagging indicators” they can be powerful sell signals. The first negative crossover on October 24 shows the 25-day and 50-day moving averages crossing below the longer term 100-day moving average – a sell signal. The second on December 12 shows the 100-day moving average crossing beneath the 200-day moving average, another sell signal. The bond remains deeply “oversold” while stocks seem significantly “overpriced,” but it is difficult to predict when the “tables will be turned” with stock prices undergoing a correction or at least a consolidation while bonds undergo a relief rally. To that end, there is a weak buy signal for the bond with a positive stochastic crossover taking place on Friday. However, any bounce higher will be met by formidable technical resistance, and it will likely take a meaningful pull-back in stock prices to fuel a recovery in bond prices leading to lower yields and lower mortgage rates

Bond prices edged higher on Monday and Tuesday only to plunge on Wednesday and Thursday before recovering slightly on Friday. The FNMA 30-year 3.5% coupon bond ($101.11, -103.2 basis points) traded within a wider 160 basis point range between a weekly intraday high of $102.44 on Wednesday and a weekly intraday low of $100.84 on Thursday before closing the week at $101.11. Friday the bond bounced marginally higher off of the 100% Fibonacci retracement support level located at $100.91. Nearest overhead resistance is found at $101.36 while stronger resistance is located at the 76.4% Fibonacci retracement level at $102.07. Overall, the bond chart shows significant technical damage has taken place since the end of September, and especially since stock prices have rocketed higher in response to the presidential election. The black circles on the chart show multiple negative moving average crossovers. Although these are “lagging indicators” they can be powerful sell signals. The first negative crossover on October 24 shows the 25-day and 50-day moving averages crossing below the longer term 100-day moving average – a sell signal. The second on December 12 shows the 100-day moving average crossing beneath the 200-day moving average, another sell signal. The bond remains deeply “oversold” while stocks seem significantly “overpriced,” but it is difficult to predict when the “tables will be turned” with stock prices undergoing a correction or at least a consolidation while bonds undergo a relief rally. To that end, there is a weak buy signal for the bond with a positive stochastic crossover taking place on Friday. However, any bounce higher will be met by formidable technical resistance, and it will likely take a meaningful pull-back in stock prices to fuel a recovery in bond prices leading to lower yields and lower mortgage rates

| Date | TimeET | Event /Report /Statistic | For | Market Expects | Prior |

| Dec 21 | 07:00 | MBA Mortgage Index | 12/17 | NA | -4.0% |

| Dec 21 | 10:00 | Existing Home Sales | Nov | 5.50M | 5.60M |

| Dec 21 | 10:30 | Crude Oil Inventories | 12/17 | NA | -2.600M |

| Dec 22 | 08:30 | 3rd Estimate for 3rd Qtr. GDP | Qtr.3 | 3.3% | 3.2% |

| Dec 22 | 08:30 | 3rd Estimate for 3rd Qtr. GDP Deflator | Qtr.3 | 1.4% | 1.4% |

| Dec 22 | 08:30 | Initial Jobless Claims | 12/17 | 256K | 254K |

| Dec 22 | 08:30 | Continuing Jobless Claims | 12/10 | NA | 2018K |

| Dec 22 | 08:30 | Durable Goods Orders | Nov | -4.5% | 4.8% |

| Dec 22 | 08:30 | Durable Goods Orders Excluding Transportation | Nov | 0.2% | 1.0% |

| Dec 22 | 09:00 | FHFA Housing Price Index | Oct | NA | 0.6% |

| Dec 22 | 10:00 | Index of Leading Economic Indicators | Nov | 0.1% | 0.1% |

| Dec 22 | 10:00 | Personal Income | Nov | 0.3% | 0.6% |

| Dec 22 | 10:00 | Personal Spending | Nov | 0.4% | 0.3% |

| Dec 22 | 10:00 | Core PCE Price Index | Nov | 0.1% | 0.1% |

| Dec 23 | 10:00 | Final Univ. of Michigan Consumer Sentiment Index | Dec | 98.2 | 98.0 |

| Dec 23 | 10:00 | New Home Sales | Nov | 573K | 563K |

Bond prices edged higher on Monday and Tuesday only to plunge on Wednesday and Thursday before recovering slightly on Friday. The FNMA 30-year 3.5% coupon bond ($101.11, -103.2 basis points) traded within a wider 160 basis point range between a weekly intraday high of $102.44 on Wednesday and a weekly intraday low of $100.84 on Thursday before closing the week at $101.11. Friday the bond bounced marginally higher off of the 100% Fibonacci retracement support level located at $100.91. Nearest overhead resistance is found at $101.36 while stronger resistance is located at the 76.4% Fibonacci retracement level at $102.07. Overall, the bond chart shows significant technical damage has taken place since the end of September, and especially since stock prices have rocketed higher in response to the presidential election. The black circles on the chart show multiple negative moving average crossovers. Although these are “lagging indicators” they can be powerful sell signals. The first negative crossover on October 24 shows the 25-day and 50-day moving averages crossing below the longer term 100-day moving average – a sell signal. The second on December 12 shows the 100-day moving average crossing beneath the 200-day moving average, another sell signal. The bond remains deeply “oversold” while stocks seem significantly “overpriced,” but it is difficult to predict when the “tables will be turned” with stock prices undergoing a correction or at least a consolidation while bonds undergo a relief rally. To that end, there is a weak buy signal for the bond with a positive stochastic crossover taking place on Friday. However, any bounce higher will be met by formidable technical resistance, and it will likely take a meaningful pull-back in stock prices to fuel a recovery in bond prices leading to lower yields and lower mortgage rates