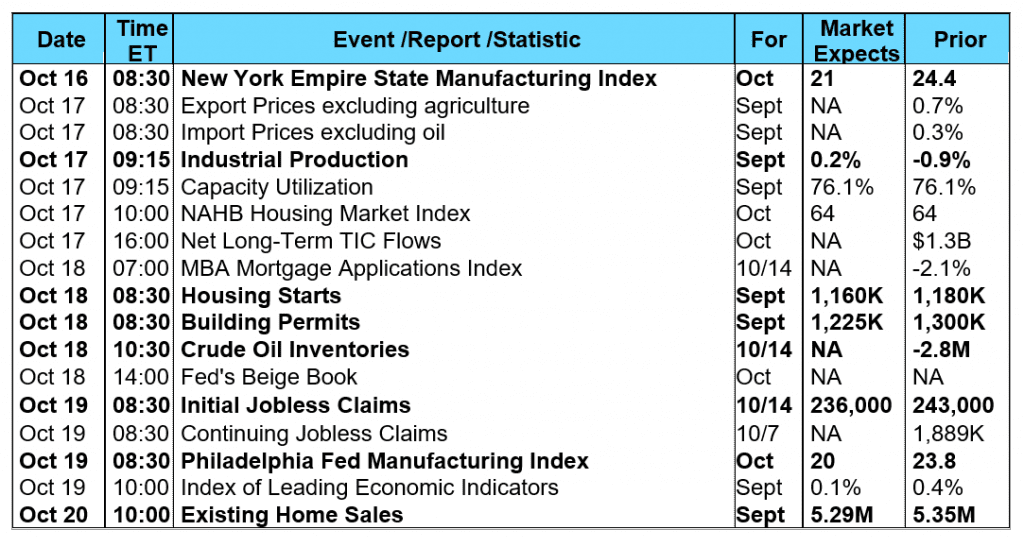

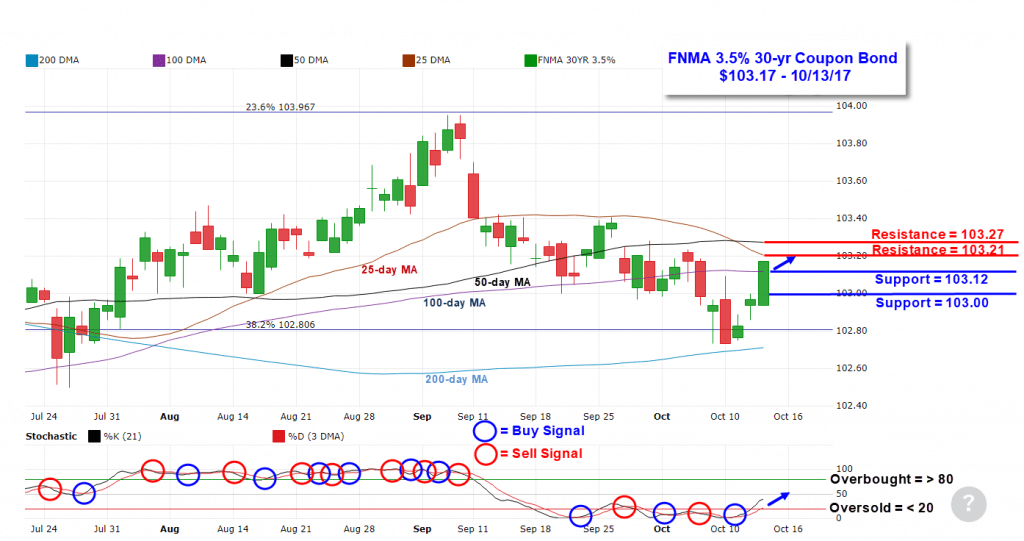

The stock market continued to advance into new record-high territory, boosted by releases from major third quarter corporate earnings reports. This past week marked the fifth consecutive weekly gain for both the Dow Jones Industrial Average and the S&P 500 Index despite a number of political and geopolitical anxieties among investors. Investor sentiment was influenced by several factors including President Trump’s executive order to revoke certain “Obamacare” regulations allowing health insurance companies to issue less comprehensive and cheaper insurance plans. Trump’s executive order also put a stop to the former Obama administration’s unconstitutional funding of subsidies that compensated health insurers for reducing premiums for low-income enrollees in state insurance exchanges. Investors also considered rumors of a potential pullout by the U.S. from the North American Free Trade Agreement (NAFTA), the possibility of another North Korean missile launch, and worried about congressional bungling on tax reform. However, there were several constructive economic reports during the week advancing both stocks and bonds. Initial Jobless Claims (243,000) fell sharply and were below the consensus forecast of 255,000. Retail Sales for September (+1.6%) exceeded expectations of +1.5%, bouncing back following August’s -0.1% decline. The boost in retail sales may be a reflection of consumers feeling better about the economy as the University of Michigan’s preliminary October reading on Consumer Sentiment reached a 13 year high at 101.1 to easily surpass the consensus forecast of 95.6 and last month's reading of 95.1. Furthermore, the latest consumer inflation data remains tame with the Consumer Price Index (CPI) coming in below the consensus forecast of 0.6% with an increase of just 0.5% in the month of September. On a year-over-year basis, CPI increased 2.2%, which is just below expectations of 2.3%. The Core CPI, which excludes food and energy prices, increased by 0.1%, which was below the consensus forecast of 0.2%. The bond-friendly inflation data helped to send bond prices higher and yields lower on Friday. In housing, mortgage application volume fell during the week ending October 6. The Mortgage Bankers Association (MBA) reported their overall seasonally adjusted Market Composite Index (application volume) declined by 2.1%. The seasonally adjusted Purchase Index decreased 0.1% from the prior week while the Refinance Index fell 4.0%. Overall, the refinance portion of mortgage activity decreased to 49.0% of total applications from 50.1% in the prior week. The adjustable-rate mortgage share of activity increased to 6.6% of total applications from 6.0%. According to the MBA, the average contract interest rate for 30-year fixed-rate mortgages with a conforming loan balance increased to 4.16% from 4.12% with points decreasing to 0.44 from 0.45. For the week, the FNMA 3.5% coupon bond gained 23.40 basis points to close at $103.172. The 10-year Treasury yield decreased 8.59 basis points to end at 2.2748%. The major stock indexes ended the week higher. The Dow Jones Industrial Average gained 98.05 points to close at 22,871.72. The NASDAQ Composite Index increased 15.62 points to close at 6,605.80 and the S&P 500 Index advanced 3.84 points to close at 2,553.17. Year to date on a total return basis, the Dow Jones Industrial Average has gained 15.73%, the NASDAQ Composite Index has advanced 22.71%, and the S&P 500 Index has added 14.04%. This past week, the national average 30-year mortgage rate fell to 3.93% from 3.99%; the 15-year mortgage rate decreased to 3.23% from 3.27%; the 5/1 ARM mortgage rate fell to 3.19% from 3.22% and the FHA 30-year rate declined to 3.50% from 3.60%. Jumbo 30-year rates decreased to 4.14% from 4.19%. Economic Calendar - for the Week of October 16, 2017 Economic reports having the greatest potential impact on the financial markets are highlighted in bold. Mortgage Rate Forecast with Chart - FNMA 30-Year 3.5% Coupon Bond The FNMA 30-year 3.5% coupon bond ($103.17, +23.40 bp) traded within a 43.8 basis point range between a weekly intraday low of $102.734 on Tuesday and a weekly intraday high of $103.172 on Friday before closing the week at $103.172 on Friday. Mortgage bond prices moved above a couple of resistance levels located at $103 and the 100-day moving average at $103.12 and these now become support levels. New resistance levels are found at the 25-day and 50-day moving averages at $103.21 and $103.27 respectively. A new buy signal was triggered on Wednesday with a positive stochastic crossover from an “oversold” position. The bond is far from “overbought” so we should see prices easily challenge overhead resistance, and a break above the identified resistance levels in the chart would lead to slightly lower mortgage interest rates.

Economic reports having the greatest potential impact on the financial markets are highlighted in bold. Mortgage Rate Forecast with Chart - FNMA 30-Year 3.5% Coupon Bond The FNMA 30-year 3.5% coupon bond ($103.17, +23.40 bp) traded within a 43.8 basis point range between a weekly intraday low of $102.734 on Tuesday and a weekly intraday high of $103.172 on Friday before closing the week at $103.172 on Friday. Mortgage bond prices moved above a couple of resistance levels located at $103 and the 100-day moving average at $103.12 and these now become support levels. New resistance levels are found at the 25-day and 50-day moving averages at $103.21 and $103.27 respectively. A new buy signal was triggered on Wednesday with a positive stochastic crossover from an “oversold” position. The bond is far from “overbought” so we should see prices easily challenge overhead resistance, and a break above the identified resistance levels in the chart would lead to slightly lower mortgage interest rates.

Economic reports having the greatest potential impact on the financial markets are highlighted in bold. Mortgage Rate Forecast with Chart - FNMA 30-Year 3.5% Coupon Bond The FNMA 30-year 3.5% coupon bond ($103.17, +23.40 bp) traded within a 43.8 basis point range between a weekly intraday low of $102.734 on Tuesday and a weekly intraday high of $103.172 on Friday before closing the week at $103.172 on Friday. Mortgage bond prices moved above a couple of resistance levels located at $103 and the 100-day moving average at $103.12 and these now become support levels. New resistance levels are found at the 25-day and 50-day moving averages at $103.21 and $103.27 respectively. A new buy signal was triggered on Wednesday with a positive stochastic crossover from an “oversold” position. The bond is far from “overbought” so we should see prices easily challenge overhead resistance, and a break above the identified resistance levels in the chart would lead to slightly lower mortgage interest rates.